Civil

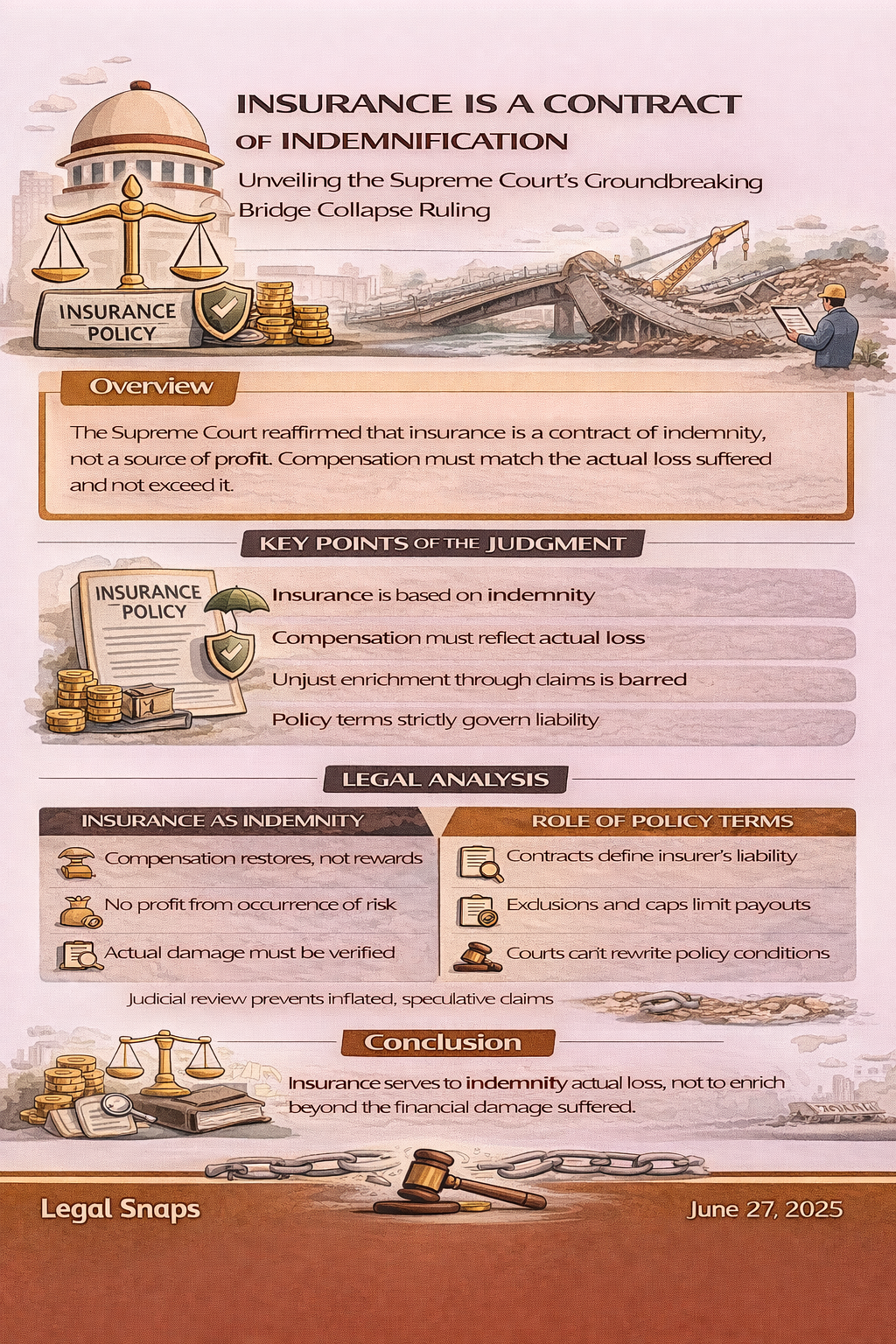

Insurance Is a Contract of Indemnification Unveiling the Supreme Court’s Groundbreaking Bridge Collapse Ruling

The Supreme Court has reaffirmed that insurance is a contract of indemnity, not profit.Compensation must strictly reflect actual financial loss.Policy terms govern liability and cannot be rewritten in equity.Insurance restores the insured it does not create windfalls.

Overview

In a significant ruling arising out of a bridge collapse dispute, the Supreme Court of India reaffirmed a foundational principle of insurance law: insurance is a contract of indemnity, not a source of profit. The Court clarified that the purpose of insurance is to compensate for actual loss suffered nothing more, nothing less.The judgment reinforces that insured parties cannot claim beyond the extent of the real financial loss and that insurers are liable only to restore the insured to the position they occupied before the damage occurred.

Key Points

- Insurance contracts are based on indemnification.

- Compensation must match actual loss suffered.

- No unjust enrichment through insurance claims.

- Policy terms strictly govern liability.

- Assessment must reflect real economic damage.

Legal Analysis

The Supreme Court reiterated that insurance contracts, unless specifically structured otherwise, are contracts of indemnity. The insurer’s obligation is to compensate for actual financial loss suffered by the insured. The occurrence of the insured event does not entitle the insured to profit or gain beyond restoration. The fundamental objective is to place the insured in the same financial position as before the loss.

A central pillar of the ruling was the principle against unjust enrichment. The Court clarified that inflated or speculative claims distort the contractual equilibrium between insurer and insured. Insurance is not a windfall mechanism, and the burden lies on the claimant to establish quantifiable and provable damage. Compensation cannot exceed demonstrable economic loss.

The Court further emphasized the binding nature of policy terms. Liability is governed strictly by the wording of the insurance contract, including exclusions, caps, and conditions precedent. Courts cannot rewrite contractual provisions under the guise of equity. Commercial certainty requires adherence to the agreed allocation of risk.

In infrastructure disputes such as the bridge collapse case, the assessment of loss must be evidence-based. Hypothetical projections, exaggerated estimates, or assumptions cannot substitute for proof. Actual repair, replacement, or economic restoration costs must be demonstrated through reliable documentation and expert valuation.

Conclusion

The Supreme Court’s ruling firmly reaffirms that insurance is a mechanism of indemnification — not compensation beyond actual loss. By rejecting inflated or excessive claims, the Court preserved contractual integrity and reinforced financial accountability within commercial transactions.The judgment strengthens the principle that insurance restores the insured to their prior position, but does not reward them with gain. In doing so, it protects both insurers and insured parties within a disciplined and predictable risk framework.