Civil

Acceptance of Insurance Proposals and Formation of Contract

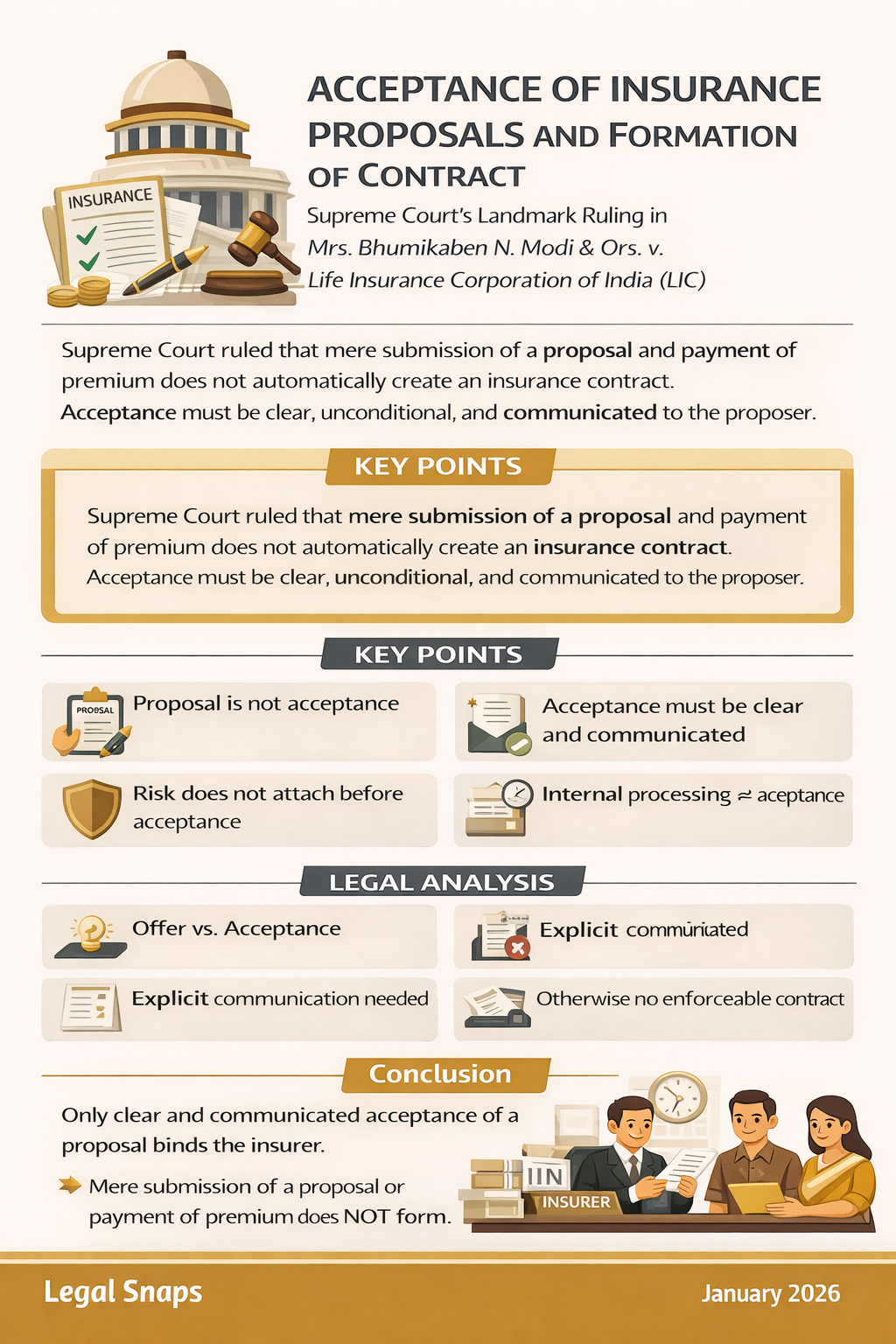

The Supreme Court has ruled that an insurance contract is formed only upon clear and communicated acceptance by the insurer. Mere submission of a proposal or payment of premium does not create liability. Acceptance must be explicit and conveyed before risk commences. The judgment reinforces foundational principles of contract law in insurance matters.

Overview

In Mrs. Bhumikaben N. Modi & Ors. v. Life Insurance Corporation of India, the Supreme Court examined when an insurance contract comes into existence. The Court clarified that mere submission of an insurance proposal and payment of premium does not automatically result in a concluded contract. Acceptance by the insurer must be clear, unconditional, and communicated to the proposer. Until such acceptance is conveyed, no binding contract of insurance is formed and no risk commences.

Key Points

- Proposal submission is not acceptance.

- Premium payment alone does not create liability.

- Acceptance must be explicit and communicated.

- Risk begins only after formal acceptance.

- Internal processing is not legal acceptance.

Analysis

The Supreme Court reaffirmed that insurance contracts are governed by general principles of contract law—offer, acceptance, and communication of acceptance. A proposal submitted by the insured constitutes an offer. Without communicated acceptance, there is no consensus ad idem and therefore no enforceable contract.

The Court distinguished clearly between proposal and acceptance. Submission of a proposal merely invites the insurer to assess risk. Acceptance requires a conscious decision by the insurer to assume liability. Internal scrutiny or administrative processing does not amount to legal acceptance unless clearly communicated.

Addressing premium payment, the Court clarified that deposit of premium is conditional upon underwriting approval. Receipt of premium does not automatically fasten liability on the insurer. If a proposal is rejected, the insurer may refund the premium without incurring contractual obligation.

The Court emphasized that acceptance must be unequivocal and communicated prior to the occurrence of the insured event. Silent or internal approval does not create binding obligations. This requirement ensures certainty, predictability, and contractual discipline in insurance transactions.

Conclusion

The Supreme Court’s decision establishes that an insurance contract arises only upon clear and communicated acceptance by the insurer. Mere proposal submission or premium payment does not create contractual liability. By reinforcing core principles of offer and acceptance, the judgment strengthens legal certainty in insurance law.